Are Your Cannabis “Write-offs” Right? A Quick Check

The title is a trick question. There are no “write-offs” in Cannabis, only COGS. You may reduce your gross receipts (essentially revenue) by your cost of goods sold (COGS). No deductions! Nearly all of the returns that we perform a complimentary review of are WRONG and potentially vulnerable to IRS audits.

Are you going to get your 2018 Cannabis tax return right? Are your past returns right?

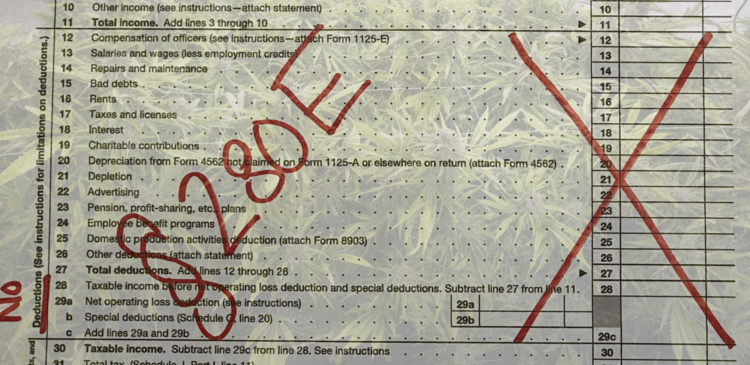

Grab your Federal tax return and look at the first page… if you have numbers in the rows designated on the far left as “deductions” there’s a good chance your tax preparer is not applying § 280E properly.

We’ll save whether your cost accounting was done properly to legally minimize your taxes under Internal Revenue Code § 1.471-3 & 11 for another post, but here’s a quick check that you can do to see if you have at least applied § 280E.

Grab your Federal tax return and look at the first page. If you file as a Partnership look to Form 1065, if a C Corp or S Corp its Form 1120 or 1120S respectively. If you’re a sole proprietor it’s not as straightforward, we’ll get to that in a moment. Now, look at the first page. If you have numbers in the rows designated on the far left as “deductions” (as in the pictures accompanying this post), there’s a good chance your tax preparer is not applying § 280E properly. Unless you meet the very narrow definition of having a separate line of business (see the CHAMP v. Commissioner of IRS court case), you should not have any numbers in the portion of your tax return with the sidebar “deductions”.

- 280E expressly disallows all deductions and credits for a business trafficking in a Schedule I or II drug, and cannabis is certainly a Schedule I drug. If your business sells cannabis products or is a separate entity that otherwise wouldn’t serve a business purpose without being intertwined with the cannabis line of business, § 280E applies. You can’t skirt § 280E with a “management company”, so take a look at those returns too.

As we mentioned, if you’re taxed as a sole proprietor, (a single member LLC would be by default), look at Schedule C of Form 1040. In Part II, “Expenses”, the instructions tell you to reduce the amounts you report as expenses by the amounts that you capitalized. Since you have to capitalize the costs associated with producing cannabis inventory to “cost of goods sold” (line 4), you shouldn’t have anything but goose eggs in the “Expenses” section. No deductions!

This is just where you start to see if your cannabis returns are at risk, but if the basics are incorrect, what else might be wrong? Your cost allocations under § 1.471-3 & 11?

If you are uncertain, a quick call with us will get you some peace of mind or point you in the right direction

{kind=link}